Some BIG Changes to Mortgage Costs Were Just Announced

The changes are in Loan Level Price Adjustments (LLPAs) imposed by Fannie Mae and Freddie Mac (the "agencies"), the two entities that guaranty a vast majority of new mortgages. LLPAs are based on loan features such as your credit score, the loan-to-value ratio, occupancy (owner vs non-owner occupied homes), and most recently, your debt-to-income ratio.

The official changes are here: https://singlefamily.fanniemae.com/media/9391/display

The down-low

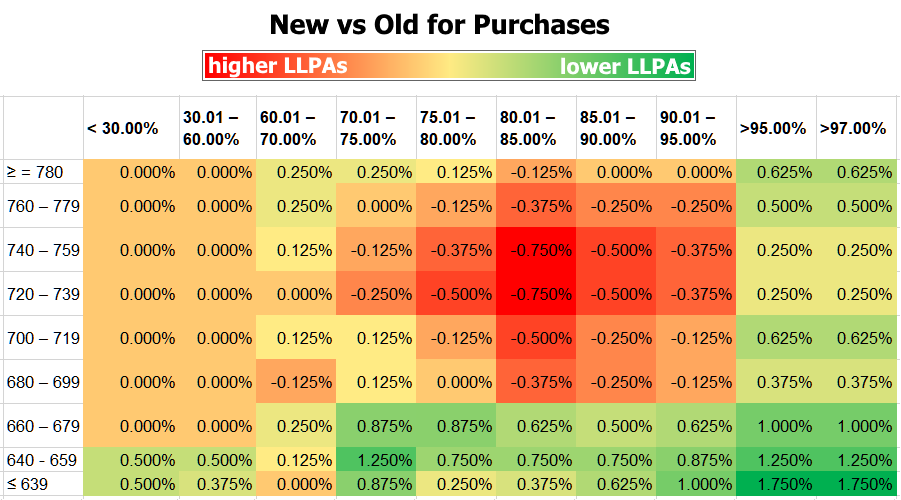

The effective penalty for having a credit score under 680 is now smaller than it was. It still costs more to have a lower score. For instance, if you have a score of 659 and are borrowing 75% of the home's value, you'll pay a fee equal to 1.5% of the loan balance whereas you'd pay no fee if you had a 780+ credit score. But before these changes, you would have paid a whopping 2.75% fee. On a hypothetical $300k loan, that's a difference of $3750 in closing costs.

Elsewhere in the spectrum, things got worse. Borrowers with higher credit scores will generally be paying a bit more than they were under the previous structure. The following chart shows the differences. Green and yellow cells show where things have become more affordable than they were. Orange and red cells = more expensive. All values refer to a percentage of the loan balance charged as an upfront fee. This doesn't necessarily come out of your pocket upfront as lenders can offer higher interest rates in some cases and pay these costs for you (but the costs are still there, and still technically being paid by you over time in the form of higher interest rates).

When does this take effect?

This applies to loans that are guaranteed by the agencies starting May 1st, 2023. That means many lenders will begin to implement the changes in March/April.

What lenders/loans does this apply to?

Any loan guaranteed by one of the agencies regardless of the lender. This is MOST loans in the US. Examples of loans that wouldn't be affected would be FHA/VA as well as certain jumbo and specialty products. "Non-conforming" loans are not impacted by this as they are not guaranteed by the agencies. A common example of a non-conforming loan would be a jumbo loan from a retail bank or credit union.